7 MIN READ/Feb 20, 2026

Summary: The blog explains how insurance agencies can improve client retention through structured workflows, operational discipline, and digitalization of P&C insurance processes. It outlines proven client retention strategies and shows how FBSPL AI tools support stronger renewals, accuracy, and long-term stability in property and casualty (P&C) insurance.

Are your renewals growing; or are you just replacing lost clients every year?

In property and casualty (P&C) insurance, growth often looks impressive on paper. New policies. New accounts. Strong production numbers. But behind the scenes? Renewal ratios fluctuate. Service teams are stretched. Clients compare quotes faster than ever.

Client retention isn’t a marketing slogan. It’s an operational outcome.

According to industry research by Bain & Company, increasing customer retention by just 5% can boost profits by 25%–95%. In insurance, that math hits even harder because acquisition costs are high. Some estimates show that acquiring a new insurance customer costs 5–7 times more than retaining an existing one.

So, the question becomes practical: how do you improve client retention without overloading your team?

In this blog, we break down five operational client retention strategies that actually work in property and casualty (P&C) insurance; and how digitalization of P&C insurance and AI tools can support them.

Understanding customer retention in the insurance industry starts with one truth: insurance is a trust business.

Clients rarely switch because of a single small mistake. They switch because of accumulated friction. Slow responses. Confusing renewals. Poor comparisons. Errors in documentation.

In property and casualty (P&C) insurance, retention is particularly sensitive because policies renew annually. That means every 12 months, your client effectively re-decides whether to stay.

Industry insights indicate a large proportion of policyholders shop around at renewal; with some surveys showing around 80% engaging in comparison behavior before renewing. (Source)

Digital aggregators have made comparisons effortless. Loyalty is no longer passive. It must be earned every cycle.

Customer retention, then, is not just about service friendliness. It’s about operational precision consisting of:

Retention is operational math. If your agency writes 1,000 policies at an average commission of $1,200 annually, a 5% drop in client retention means 50 lost policies; $60,000 in revenue erosion. That doesn’t include cross-sell opportunities or lifetime value.

Small percentage shifts matter.

And here’s something agencies functioning in USA, CA and even globally often overlook: clients judge competence through clarity. If renewal comparisons are confusing or proposals look inconsistent, confidence drops, quietly.

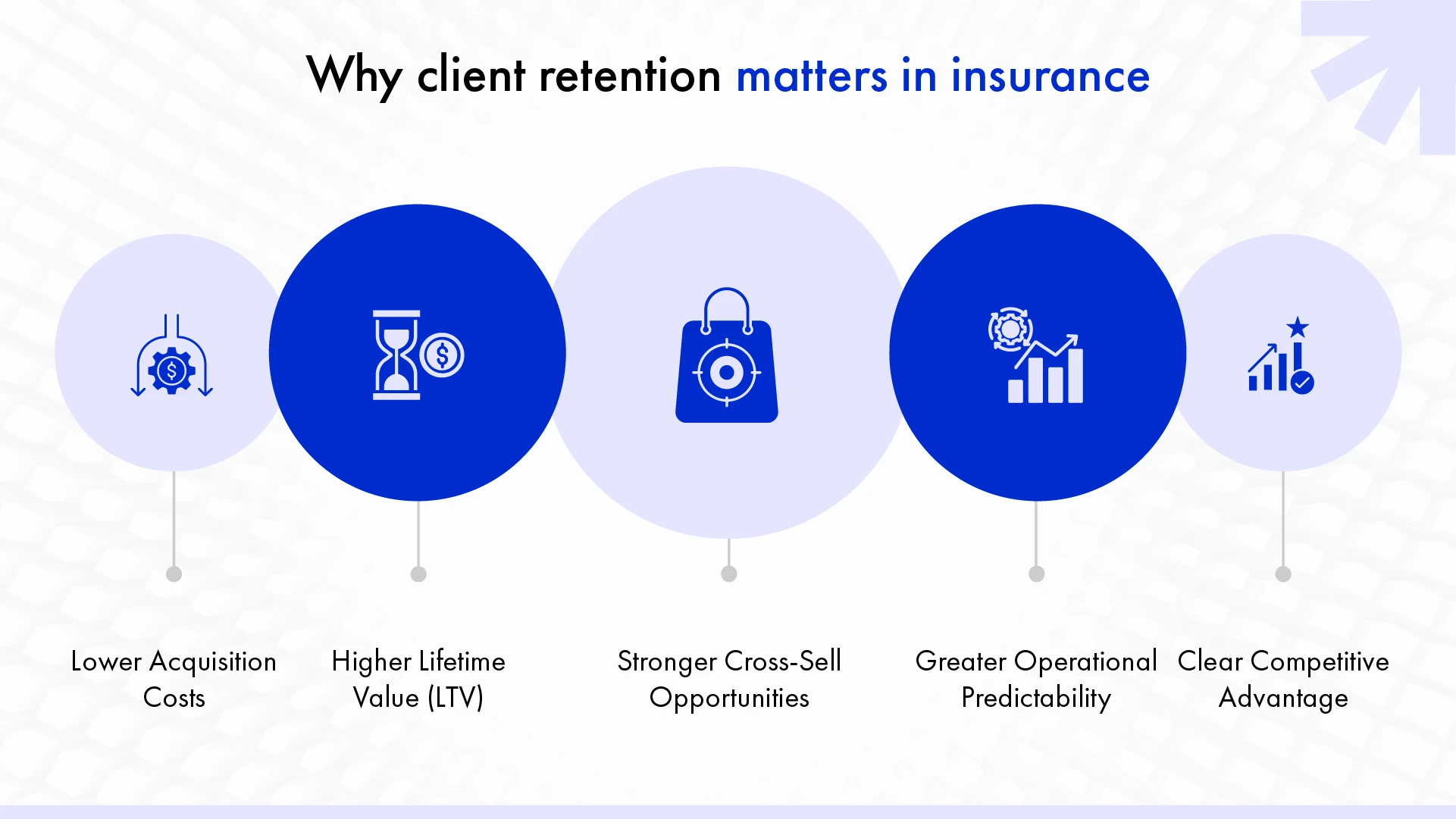

Why is client retention important in the insurance business? Because retention stabilizes revenue, reduces acquisition pressure, and increases long-term agency valuation.

Let’s break it down practically.

Client retention is not just defensive. It is strategic. And honestly? Agencies that ignore retention often end up in a constant production treadmill; running hard, moving slowly.

Client retention in insurance is about more than just policy renewals — it’s about building long-term relationships based on trust, responsiveness, and consistent value. Agencies that focus on proactive communication and personalized service are far more likely to retain clients over time. In today’s competitive insurance landscape, improving retention requires a strategic approach. From leveraging technology to enhancing client engagement, agencies must continuously adapt to meet evolving customer expectations.

Here are proven strategies insurance agencies can use to improve client retention:

Renewal season is decision season. Clients want clarity.

When coverage differences aren’t clearly explained, uncertainty creeps in. Confusion increases shopping behavior.

Agencies that standardize side-by-side renewal comparisons see stronger retention because clients understand value, not just price.

Clear comparison reduces friction. It builds trust. And trust renews policies.

Speed matters. According to J.D. Power studies, insurers with faster service resolution show significantly higher satisfaction scores.

Delays create doubt. Even if coverage is solid.

Reducing endorsement turnaround from 48 hours to same-day handling can materially improve client perception. Operational math again.

Manual review processes introduce risk. Missed endorsements. Incorrect limits. Formatting inconsistencies.

Digitalization of P&C insurance processes; especially document processing and data extraction; significantly reduces review mistakes. Studies show automation can reduce administrative errors by 30–50% in financial services workflows.

Higher accuracy can result in stronger retention confidence.

First impressions influence long-term loyalty. If onboarding requires repeated emails, incomplete forms, or unclear data collection, clients start with frustration.

Smart intake systems streamline this experience and reduce friction at the beginning of the relationship. Boosting client retention from day one.

Clear, branded, side-by-side insurance comparisons help clients make confident decisions. Inconsistent formatting or rushed presentation reduces perceived value, even if the coverage is excellent.

Small presentation gaps. Big perception impact.

Agencies that treat proposals as strategic documents, not just attachments, often report stronger close rates and improved client retention over time.

One small operational shift can compound across hundreds of accounts.

Retention improves when workflows are structured.

FBSPL’s tool suite supports three high-impact areas that directly influence renewal confidence and client experience.

PolicyLens automates extraction and side-by-side comparisons of premiums, limits, deductibles, endorsements, and coverage changes.

Key impact areas:

When renewal conversations include precise, structured comparisons, clients feel informed.

And there’s a practical benefit: faster reviews allow teams to focus on advisory discussions instead of document checking. That shift matters.

Proposals often take 30–60 minutes to format and finalize. Multiply that by 200 renewals.

ProposalOne extracts quote data and transforms it into polished, client-ready proposals instantly; complete with side-by-side coverage comparisons.

Retention benefit:

When proposals look professional and structured, clients perceive competence.

Perception influences renewal decisions more than agencies sometimes realize.

PhoenixQ replaces static forms with conversational data collection.

Instead of email back-and-forth, clients provide information through guided, real-time validated interactions.

Operational advantages:

Improved onboarding improves long-term loyalty.

And here’s the bigger picture: digitalization of P&C insurance doesn’t replace relationships. It strengthens them by removing administrative friction. That’s the difference.

Client retention strategies only deliver consistent results when the underlying operations are structured to support them. Without process stability, even strong client relationships can weaken under pressure during peak renewal periods.

According to Accenture, insurers that invest significantly in digital capabilities tend to outperform their peers in both customer satisfaction and cost efficiency. That advantage does not come from technology alone, but from reduced variability across servicing, renewals, and documentation workflows.

When variability declines, errors decrease. As errors decrease, trust strengthens. And over time, that trust compounds into measurable retention stability.

The reality many agencies quietly recognize is this: most clients are not lost purely because of pricing differences. They leave due to accumulated operational friction; delayed responses, unclear comparisons, and inconsistent documentation.

Address the friction systematically, and retention improves as a natural outcome rather than a forced objective.

Client retention in property and casualty (P&C) insurance comes down to disciplined execution.

It is built through:

How can insurance agencies improve client retention?

By reducing errors, shortening turnaround times, and improving clarity across every renewal interaction.

FBSPL supports this through structured digitalization of P&C insurance processes and purpose-built AI tools that strengthen policy reviews, proposals, and intake accuracy. Practical improvements. Measurable impact.

Insights and analysis from our industry experts.

Most independent agencies target 85–92% retention depending on business mix and market segment.