How AI in insurance transforms operational efficiency for MGAs | A complete guide

18 MIN READ/Aug 28, 2025

Every MGA knows the feeling: the inbox swells before 9 a.m., submissions arrive in six formats (none of them clean), and the team spends half the day deciding which files deserve attention first. By noon, an underwriter is still hunting for a loss run hidden in a broker’s thread. A claims note sits untagged. The policy admin queue has three simple endorsements that somehow became complicated because data lives in five places.

This isn’t a lack of effort. It’s the cost of scattered processes and legacy decisions that once made sense. The market, meanwhile, moves faster. Retail agents expect quick answers. Carriers want precision. Compliance never sleeps.

Here’s where AI in insurance becomes practical, not theoretical. Think less “moonshot,” more “better Tuesday.” Tools that read messy emails and sort what matters. Models that rank submissions by fit and likely close rate. Systems that turn free-form notes into structured data you can actually use. That’s AI for operational efficiency, tangible improvements inside the real work of an AI in insurance business.

Pair that with experienced external support, insurance BPO teams that know bordereaux from binders, and you get a workable plan: automate the grunt work, keep judgment with your experts, and outsource insurance process management where scale and accuracy matter most. In short, use AI for insurance operations to free capacity, then direct that capacity toward underwriting quality, distribution, and loss ratio.

In this guide, we’ll map exactly how MGAs can do it: what to automate first, where the big gains hide, the pitfalls to avoid, and how outsourcing fits alongside AI so the whole operation runs cleaner and faster, without losing the human decisions that protect the book.

The MGA challenge: Building programs while battling bottlenecks

Why MGAs matter?

MGAs aren’t just intermediaries. They’re the builders who turn carrier capacity into useful coverage for specific niches, contractors in three states, coastal property with particular wind exposures, high-hazard manufacturers that need more than a generic questionnaire. An MGA curates appetite, shapes wording, and keeps the distribution engine humming with dozens of relationships that span brokers, TPAs, inspection vendors, and carriers.

Where time disappears?

Ask any MGA where the day goes and you’ll hear the same handful of culprits:

- Submission intake: PDFs, email attachments, and spreadsheets arrive half-complete. Someone has to sort, read, and key the essentials. That someone is usually your most expensive talent.

- Appetite matching: Deciding who should see what is still tribal knowledge, “Jess knows which carrier will hate that roof age.” When Jess is out, the queue stalls.

- Underwriting artifacts: Loss runs missing a year. Data buried in a PDF. Values that don’t reconcile. Your team spends minutes, then hours, reconstructing facts.

- Endorsements and mid-term changes: These look simple until you trace the data across policy admin, the rating workbook, and the carrier reporting feed.

- Compliance: The monthly/quarterly sprint to align fields and formats across carriers is thankless and high stakes.

- Claims coordination: First Notice of Loss arrives by phone, email, portal. Notes get long; context gets lost; follow-ups slip.

- Sales support: Producers need fast, accurate comparisons. Marketing needs performance data that lives everywhere except in one place.

What that friction costs?

Every manual step creates delay and leakage. Submissions age while competitors quote. Good risks sit at the bottom of the pile because they arrived messier than the rest. Teams burn cycles on re-work. Leaders make decisions with stale numbers. The book grows, but not with the mix you wanted.

Where AI actually fits?

This is not about replacing underwriters; it’s about replacing the scavenger hunt. AI in insurance can read an inbox at scale, convert unstructured files into consistent fields, tag missing items, and point attention at the 20% of cases that deserve 80% of your expertise. That’s the heart of AI for operational efficiency. And when you complement it with a capable insurance BPO, to outsource insurance process tasks like data prep, document chase-downs, or repetitive endorsements, you get throughput without sacrificing control. For many MGAs, the breakthrough comes from this pairing: smart automation + disciplined execution.

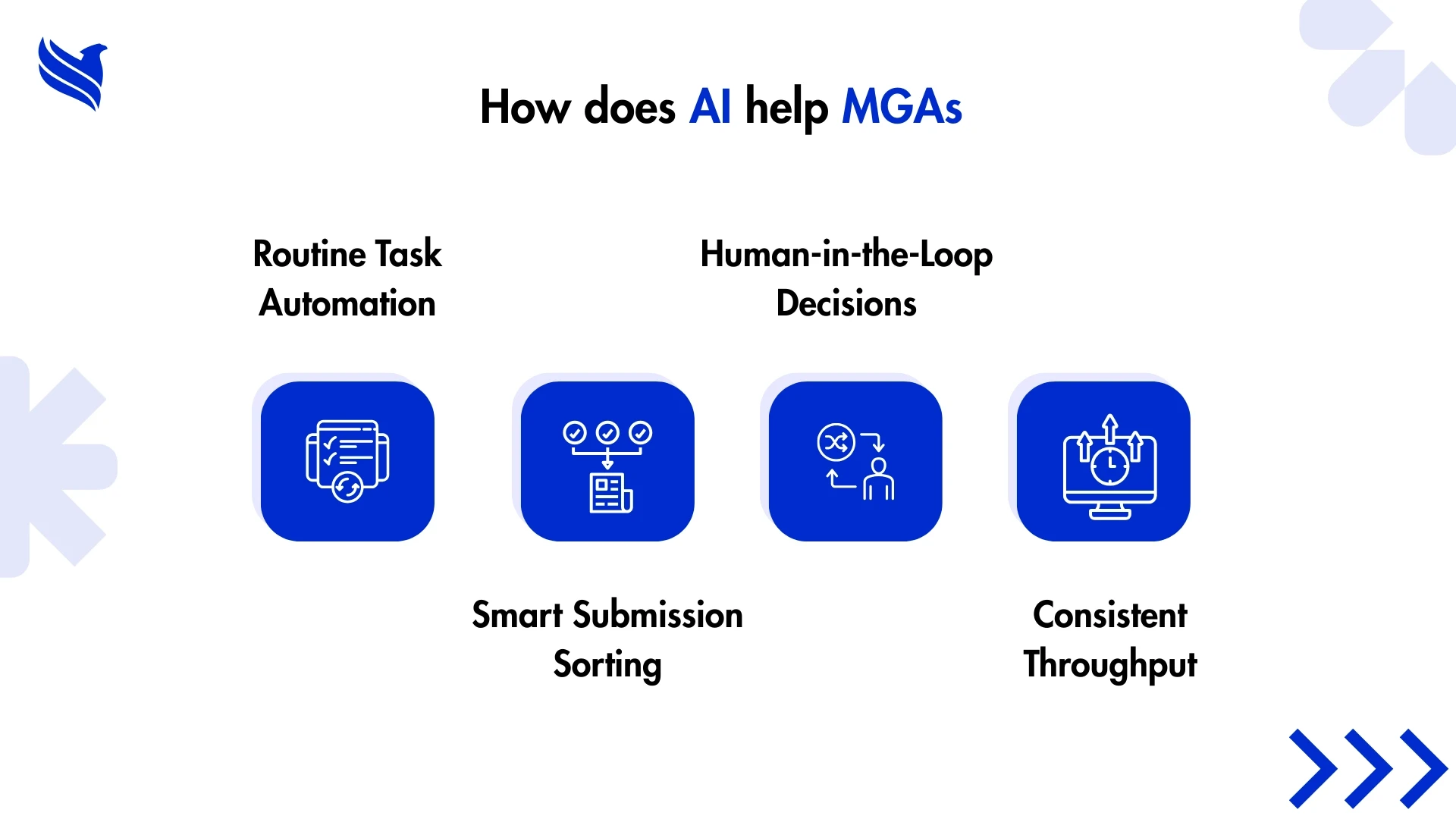

AI in action: Taking the load off MGA operations

If you watched MGAs five years ago and then again today, the change is subtle and messy. The first wave of adoption isn’t about replacing people; it is about giving them less of the tedious, attention-sapping stuff that makes good underwriters sound like data-entry clerks. That quiet, practical entry point is what’s driven the real rise of AI in insurance operations.Here’s how that happened in plain terms. A few tasks were obvious candidates for automation: reading messy PDFs, pulling the right numbers out of loss runs, matching a submission to a carrier appetite. Vendors built models that could do these things well enough to make finance and operations teams comfortable. Once the technology proved itself on those small wins, larger pieces followed, routing decisions, simple risk scoring, predictive flags for claims that need early intervention.

Two forces pushed this forward.

First, the data itself improved. MGAs kept feeding the systems with corrections, human overrides, and exceptions. The algorithm learned what mattered and what didn’t. Second, the business case became immediate: cut the time a binder sits in the queue from days to hours, reduce avoidable chargebacks, free senior underwriters to focus on bigger, nuanced decisions. That’s AI for operational efficiency in action, not a magic wand, but a tool that shifts the work mix.

A few practical patterns you’ll see across MGAs:

- Intake-first projects. Start by using models to read emails, extract coverages, and flag missing documents. This alone clears a huge backlog and reduces the number of times a human has to look at a file before it’s usable.

- Decision support, not replacement. Systems surface recommended actions and confidence scores. Humans continue to take the final call. The result: speed without reckless automation.

- Focused risk scoring. Instead of building a single, monolithic model, teams create thin models for specific questions; “Is this submission likely to be declined?” or “Does this claim warrant immediate reserve increase?” These narrow models are easier to validate and faster to deploy.

- Feedback loops. The best implementations hardwire the corrections back into training data: when an underwriter changes a model’s suggestion, that change becomes the next lesson.

This is also the point where other technologies fold in. Sensors and telematics started influencing underwriting decisions, an area where machine inputs meet human judgement. If you want a deeper look at how connected devices are changing underwriting and risk oversight, read Smart insurance: How AI and IoT are reshaping underwriting and risk management. That mix, device data feeding models, and teams using the outputs to price or decline risk, is a concrete example of How is AI transforming the insurance industry in real operational terms.

Finally, adoption often comes with a parallel decision about scale: do you build in-house or partner? Many MGAs find a hybrid path sensible. Build core differentiators internally; outsource repeatable, high-volume tasks to specialists who combine human teams and automation, the classic insurance BPO approach. When you outsource insurance process management, you get scale and disciplined execution without stretching internal staff.

The rise we’re describing isn’t theoretical. It’s a series of small operational moves, intake automation, focused scoring, and human-in-the-loop decisioning, that add up to material capacity gains for MGAs. The trick is to pick the low-hanging fruit, measure it, and then expand.

Turning hours saved into smarter operations

Put a stopwatch on a typical underwriting pathway and you’ll see where time leaks out: file triage, manual data entry, chasing missing documents, and comparing rates across carriers. How does AI improve operational efficiency? By attacking those specific points with tools that read, categorize, and prioritize so people can do the parts only people should do.

Here are concrete ways AI cuts friction, and how you can think about applying each one.

Reading and structuring information.

Unstructured documents are thieves of time. Modern models read PDFs, convert handwriting or scanned loss runs into usable fields, and assemble a submission packet that an underwriter can act on. That means fewer “please resend” emails and fewer back-and-forths.Prioritization and routing.

Not all submissions are equal. Algorithms can rank opportunities by likely fit and expected margin, so the best ones get eyes first. That reduces the chance a high-quality risk sits buried and increases the speed to quote, which producers notice immediately.Automated checks and validation.

Models spot mismatches: a policy limit that doesn’t match the application, missing loss history, or exposures that contradict the stated occupancy. Flagging these early prevents downstream corrections and billing headaches.Smart templating and proposal generation.

Drafting proposals used to be a repetitive chore. Today, insurance proposal generation tools can pull the right clause language, price scenarios, and bind-ready documents in a fraction of the time. Smart AI proposal generation solutions shrink turn-around time and lift conversion rates because producers get answers that look and feel professional faster.Claims triage and early intervention.

For MGAs that manage claims workflows, quick identification of high-severity files matters. Models that analyze initial reports and historical patterns can flag cases that need immediate adjuster attention or specialist review, reducing leakage and reserve mistakes.Reconciliation and reporting.

Monthly carrier feeds and commission statements are a massive drain. Automation that matches entries across systems or pulls exceptions for human review turns a multi-day slog into a focused exception-management task. This is the classic place where insurance BPOs provide value: they can take on routine reconciliation with automation layered on top, delivering clean, auditable outputs.Human capacity reallocation.

Most importantly, AI often returns time to the best-paid people. Rather than typing fields or chasing docs, underwriters are freed to negotiate terms, refine appetite, and mentor juniors. That shift changes culture; it makes the job more engaging and the book smarter.

A small, realistic example: an MGA introduces an intake AI and a hands-off document-prep partner. Submissions that used to require 25 minutes of prep now need 3 mins, mostly to handle edge cases. The underwriters’ queue clears faster. Producers get quotes sooner. Renewal retention improves because renewals are handled proactively rather than reactively. None of that required replacing humans; it required reassigning what humans do best.

Where to start? Pick the choke point that causes the most daily irritation, intake or endorsements, and aim for measurable wins. Use short pilots, keep the humans in the loop, and make sure someone owns the feedback into models and process changes.

That’s the practical promise of AI; not an abstract productivity claim, but reclaimed hours, clearer data, and faster, better decisions. When MGAs combine these capabilities with disciplined operations, whether done internally or through an insurance BPO, they move from firefighting to planning. And that’s the moment operational improvement turns into a competitive advantage.

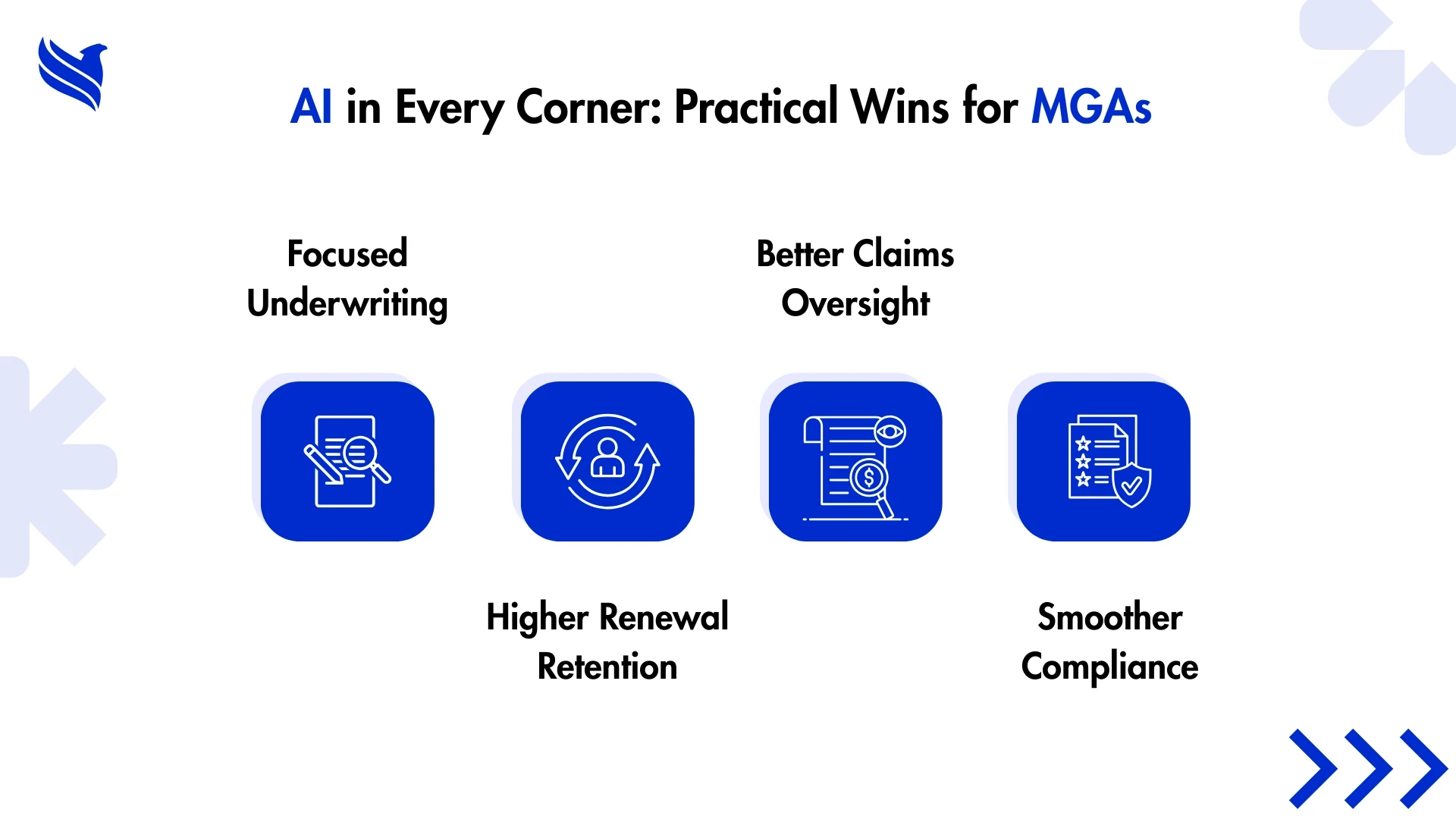

Real results: How AI drives measurable MGA performance

The easiest way to misunderstand AI is to think of it as a single tool. It’s better to think of AI as a set of small, purpose-built assistants, each one handling a specific kind of grunt work so your experts can focus on judgment calls.

Here’s how that plays out across core MGA functions:

- Underwriting Support: AI can scan a new submission, identify missing elements, and cross-check against carrier appetite rules in seconds. Instead of an assistant underwriter spending half an hour on prep, the file arrives clean and ranked for review. That shift alone is worth days of capacity each month.

- Distribution and Broker Engagement: AI models can score which brokers bring in the highest-quality submissions, not just in volume, but in profitability. MGAs can then adjust marketing efforts and relationship management accordingly.

- Renewals: Rather than wait for a renewal to appear in the system, AI tools can flag accounts at risk of churn based on broker behavior, market changes, or client-specific factors. This means your team can re-quote early, adjust terms, and keep the account.

- Claims Oversight: For MGAs with claims authority, early detection matters. AI reads FNOL (First Notice of Loss) descriptions, compares them to historical patterns, and flags potential high-loss events. This allows claims managers to prioritize their adjusters’ time effectively.

- Compliance and Reporting: Regulatory filings are historically high-friction areas. AI can match and validate data fields, flag anomalies, and compile reports ready for human sign-off.

- Proposal and Marketing Material Generation: AI-driven proposal generation tools that can draft tailored proposals, drawing from your specific wordings, endorsements, and pricing logic, help insurers deliver polished quotes faster. That’s not just speed; it’s professionalism that closes deals.

MGAs operate on thin margins and tight timelines. The most successful ones don’t try to automate the soul out of the business; they automate the repetitive mechanics so the human brain can focus on the nuanced calls. That’s how AI helps MGAs, not by replacing the MGA, but by making the MGA sharper and faster.

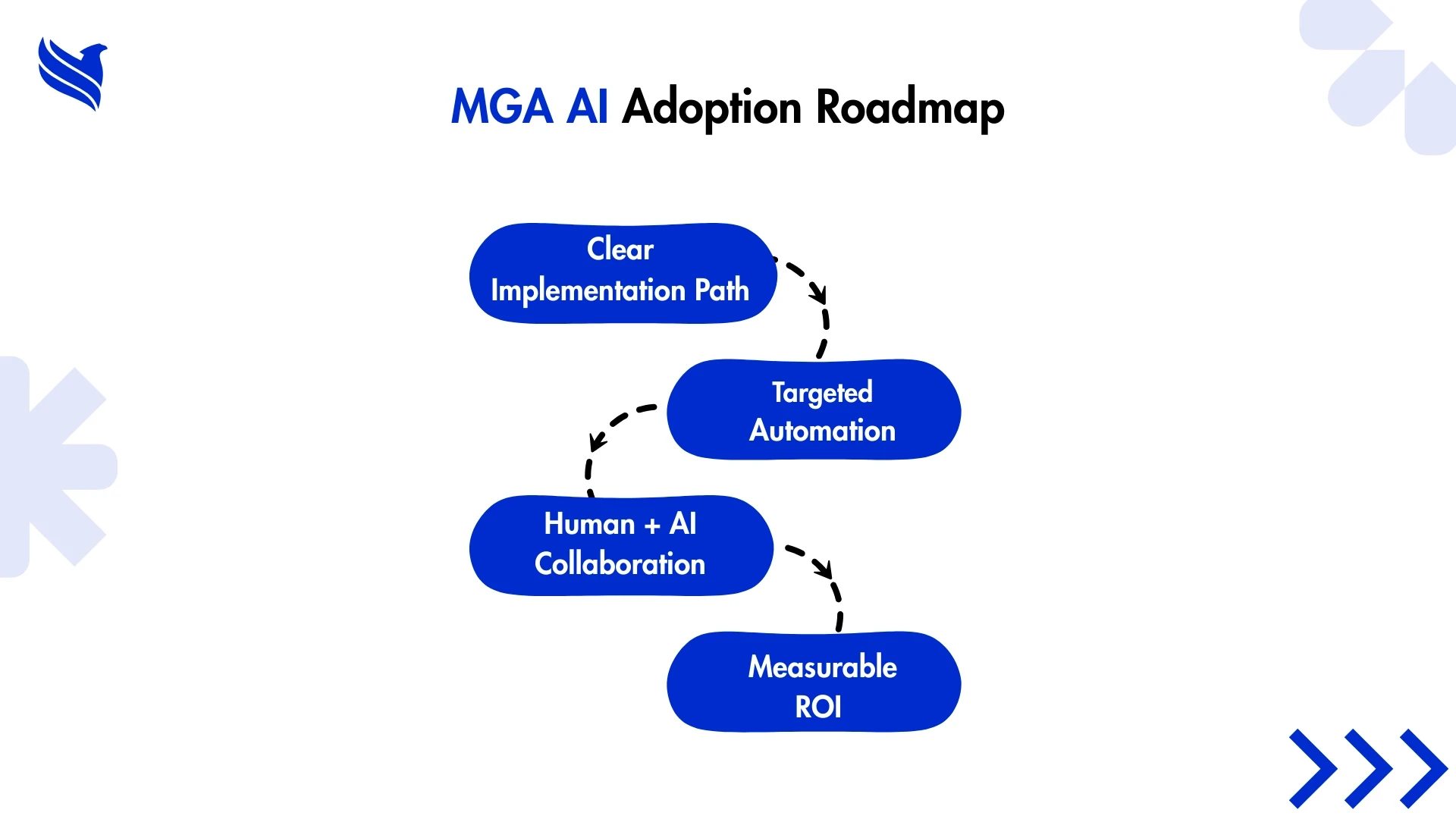

Building an AI playbook for MGA operations

Adopting AI for insurance operations isn’t about chasing shiny tools; it’s about sequencing the right steps so the benefits stick.

Here’s a practical playbook:

Step 1: Map the Friction

Spend a week documenting where delays occur; submission review, endorsements, claims notes. Track how much time and how many touches each step takes.

Step 2: Match AI to Choke Points

Look for the bottlenecks that involve repetitive, rules-based work and heavy data handling. These are your automation sweet spots.

Step 3: Pilot Narrowly

Instead of trying to “transform” the whole operation, pick one workflow (e.g., submission intake). Roll out AI to that process only, measure the results, and adjust before expanding.

Step 4: Keep Humans in the Loop

Models make mistakes; context matters. Build workflows so an underwriter or processor can override AI decisions quickly, and feed that override back into the model for learning.

Step 5: Pair with the Right Partner

If you don’t have the internal bandwidth to implement and monitor AI tools, work with an insurance BPO to outsource insurance process management. The partner can handle repetitive work while you retain control over underwriting judgment.

Step 6: Create Feedback Loops

Your AI is only as good as the corrections it receives. Make it easy for staff to log errors or exceptions, and use that data to refine both the model and the process.

Step 7: Integrate, Don’t Isolate

AI tools should plug into your existing policy admin, CRM, and accounting systems, not create a new island of data. Integration prevents double entry and keeps the whole picture in one place.

This is a playbook you can execute without derailing your business. Start small, prove the value, scale intentionally.

AI-driven marketing and lead generation for MGAs

AI isn’t just for underwriting and operations. It’s also changing how MGAs approach the front end of the business: marketing and lead generation.

- Audience Intelligence: Models can analyze your historical book and find patterns: which industries, geographies, and broker relationships bring in profitable accounts. This turns marketing from a shotgun blast into a rifle shot.

- Broker Prioritization: AI can rank brokers based on submission quality, speed to bind, and retention rates. Your marketing team can then spend their energy where the ROI is highest.

- Content and Proposal Customization: Instead of sending generic brochures, AI tools can produce marketing pieces tailored to the broker’s region, industry, and past placements. That level of relevance improves open rates and meeting conversions.

- Predictive Timing: Algorithms can flag when a broker is likely to have accounts coming up for renewal or when certain industries are in a buying window. This allows your producers to reach out at the right moment, not months too late.

- Lead Scoring: For MGAs that market directly to insureds in niche lines, AI can score leads based on likelihood to bind, so your team focuses on the top tier first.

Marketing is where speed and precision matter equally. AI gives MGAs the data to be precise, and, when tied into proposal automation, the ability to respond while the lead is still warm.

Future trends and opportunities in AI for MGAs

We’re past the “will AI matter?” phase. The next questions are: How is AI transforming the insurance industry next, and where can MGAs capture the upside?

A few trends worth watching:

- Richer Data Sources: The next wave isn’t just policy and claims data. It’s IoT devices, satellite imagery, and real-time business intelligence feeding into MGA underwriting models. We’re already seeing MGAs use property imagery to assess roof condition before renewal, without an inspection.

- Embedded AI in Core Systems: Soon, you won’t need separate AI tools; your policy admin, CRM, and claims system will have AI built in. This makes adoption easier but also means MGAs must understand how those embedded models work, and where to challenge them.

- Automated Compliance Monitoring: With regulatory changes accelerating, AI will monitor your book for emerging compliance risks in real time, adjusting workflows before a problem becomes a violation.

- Dynamic Pricing Models: More MGAs will experiment with models that adjust pricing based on live risk data; for example, real-time crime stats for inland marine, or weather forecasts for property. This brings the underwriting mindset closer to continuous monitoring than static pricing.

The takeaway: the opportunity isn’t just in adopting AI tools, but in building a culture that expects constant iteration. The MGAs who thrive will be the ones who treat AI like any other operational resource; budgeted, measured, and refined.

Where outsourcing meets AI: A force multiplier for MGAs

Even the most forward-thinking MGA can run into a hard limit: people. You can have the best AI for insurance operations, but if your internal team is already running at capacity, the gains stay trapped on paper. That’s where outsourcing stops being a cost conversation and becomes an operational one.

A seasoned insurance BPO partner doesn’t just “do the tasks you don’t want.” The right one knows MGA workflows, understands carrier quirks, and can integrate with your AI systems so automation and human effort work in tandem. Think about what happens when you outsource insurance process management with AI embedded:

- AI reads the submission, extracts the data, and flags missing items.

- The outsourced team retrieves those missing documents, validates fields, and pushes a clean file to underwriting.

- AI runs appetite checks and risk scoring; the partner handles any low-complexity endorsement or policy issuance work that follows.

In practice, this combination acts like an elastic workforce. When your new business spikes or renewal season hits, you don’t scramble for temps or burn out staff. You flex capacity up with your partner, and when volume drops, you scale back without carrying idle salaries.

Outsourcing also helps on the innovation side. Many MGAs find that BPO partners already use specialized AI tools in their own operations, meaning you get technology uplift without paying for every license yourself. Some even manage model training for you, feeding back human-reviewed data so your AI stays sharp over time.

For MGAs under pressure to grow without inflating headcount, this hybrid approach, automation plus trusted external execution, isn’t just efficient. It’s a safeguard against operational drag.

Conclusion: Turning efficiency into advantage

MGAs have always been builders, of programs, relationships, and market niches that carriers alone couldn’t reach. But in a market that demands faster turnarounds, sharper risk selection, and tighter compliance, building now requires new tools.

The rise of AI in insurance business has given MGAs a way to reclaim lost hours, improve accuracy, and make better use of their people. The real advantage comes when you combine that AI with targeted outsource insurance process support, letting automation handle the sorting and scoring, and letting skilled external teams handle the repeatable execution. Together, they give you more capacity without more headcount, and more insight without more noise.

At FBSPL, we’ve seen this in action across multiple MGA clients, not just in underwriting and policy admin, but in insurance proposal generation itself. Our AI proposal generator tool takes your appetite, pricing logic, and preferred wording, and turns them into polished, ready-to-send proposals in a fraction of the time. It’s a direct, measurable way to turn operational efficiency into deal wins, the kind of advantage you feel in your close rates, not just in a process chart.

If you’re ready to explore how AI and outsourcing can work together to take the grind out of your MGA operations, we can help. FBSPL brings the tech, the people, and the process know-how to move you from “keeping up” to leading.

Expert Contributor

Insights and analysis from our industry experts.

.png&w=3840&q=75)