How to choose the right insurance back-office outsourcing partner in the US

8 MIN READ/Jun 15, 2026

Summary: Choosing the right insurance back-office outsourcing partner requires more than comparing costs. Insurers should evaluate industry expertise, technology capabilities, compliance frameworks, scalability, and proven outcomes. A strategic partner can improve operational efficiency, support growth, reduce risk, and enhance customer experience.

Across the US insurance landscape, a quiet but costly crisis is unfolding. Policy administration backlogs pile up. Claims processing drags into days. Compliance deadlines loom while skilled staff are buried in repetitive, manual workflows. Leadership teams, stretched thin between client servicing and regulatory obligations, find themselves with little bandwidth left to think strategically.

This isn't a resource problem. It's a structural one.

The answer that a growing number of insurers; from regional carriers to MGAs; are turning to is insurance back-office outsourcing. But here's where many organizations stumble: they treat the search for an outsourcing partner like a procurement exercise, comparing rates and turnaround times rather than evaluating strategic fit, technology depth, and long-term transformation potential.

The reality is this; the right insurance back-office outsourcing partner doesn't just absorb your workload. They rebuild the way your operation runs.

This blog walks you through exactly how to make that decision.

The scale of the shift: Why insurance BPO is a strategic imperative

The numbers tell a compelling story. According to IMARC Group's Insurance BPO Market Report, the global insurance business process outsourcing market was valued at USD 7.47 billion in 2024 and is projected to reach USD 10.40 billion by 2033, growing at a CAGR of 3.57%; with North America commanding over 35.8% of global market share.

This isn't a trend. It's a structural transformation in how insurance operations are being built.

The drivers behind this shift are deeply operational: rising labor costs, increasing regulatory complexity, talent shortages, and the accelerating demand for innovative insurance technology solutions that most in-house teams simply can't keep pace with.

What falls under core insurance back-office services?

Before evaluating any outsourcing partner, decision-makers must have clarity on the scope. Core insurance back-office services typically include:

- Policy administration & endorsements — issuance, modifications, renewals, and cancellation processing

- Claims processing & management — first notice of loss (FNOL), documentation review, adjudication support, and settlement coordination

- Underwriting support — risk data gathering, submission intake, quote preparation, and loss run analysis

- Premium accounting & reconciliation — billing, payment posting, and reconciliation workflows

- Compliance & regulatory reporting — filings, audit support, and documentation management

- Data entry & document management — indexing, digitization, and database management

- Customer service & renewal management — renewal follow-ups, certificate issuance, and policyholder correspondence

The volume and complexity of these functions make them ideal candidates for outsourcing; not to offload responsibility, but to execute them with greater precision, speed, and compliance adherence than in-house generalists can deliver.

The real challenges driving insurers to outsource

Understanding why agencies and carriers are outsourcing helps clarify what to look for in a partner. The most common pain points include:

1. Operational bottlenecks that drain revenue

Manual workflows create processing delays that directly affect client satisfaction and renewal rates. When your team spends more time on data entry than relationship building, growth slows.

2. Talent gaps and workforce instability

Insurance back-office roles are increasingly hard to staff in-house. Training cycles are long, attrition is high, and specialized expertise; such as surplus lines compliance or reinsurance accounting; is rare.

3. Technology lag

Many insurers are still operating on legacy systems. A capable BPO provider brings innovative insurance technology solutions; including AI-assisted processing, RPA (robotic process automation), and integrated workflow tools; without requiring the insurer to fund those capabilities independently.

4. Compliance pressure

State-specific regulations, changing DOI requirements, and evolving data privacy laws create a compliance overhead that demands dedicated expertise, not ad hoc attention.

5. Scalability constraints

Seasonal volume spikes; open enrollment periods, catastrophe events, renewal cycles; strain in-house teams. Back-office outsourcing provides the elasticity to scale without permanent headcount increases.

How to choose the right insurance outsourcing partner

This is where strategy must replace intuition. Here are the critical evaluation criteria:

1. Deep insurance domain expertise — not just BPO

The first filter is specialization. There are many capable BPO providers in the market; but insurance is a domain with its own language, workflows, regulatory anatomy, and risk exposure. Your partner must understand carrier relationships, policy lifecycle management, state-specific compliance nuances, and the operational difference between P&C, life, health, and commercial lines.

Ask directly: How many dedicated insurance back-office workflows does your team manage today? What lines of business do you specialize in?

2. Technology stack and process automation capability

According to Deloitte's 2024 Global Outsourcing Survey, 83% of executives are already leveraging AI as part of their outsourced services, and 80% are planning to maintain or increase their investment in third-party outsourcing.

This signals that AI-enabled outsourcing is no longer an advanced use case; it's table stakes. The right partner should demonstrate RPA deployment, intelligent document processing, workflow automation, and integration capability with platforms like Applied Epic, Vertafore, Guidewire, or Duck Creek.

3. Compliance Architecture and Data Security

Any credible insurance back-office support partner operating in the US market must demonstrate:

- SOC 2 Type II certification

- HIPAA compliance (for health-adjacent data)

- E&O coverage and clear liability frameworks

- State-specific regulatory fluency

- Data governance protocols aligned with NAIC model laws

Compliance isn't a feature. In insurance, it's the floor.

4. Measurable SLAs and transparent reporting

The outsourcing process should come with contractual clarity. Look for partners who offer defined turnaround time SLAs, error rate benchmarks, processing volume guarantees, and real-time dashboard visibility. Vague commitments like "high accuracy" and "fast turnaround" are not accountability frameworks.

5. Scalability and transition methodology

How does the partner handle volume spikes? What does their onboarding process look like? A robust transition methodology; covering knowledge transfer, workflow documentation, parallel processing phases, and dedicated account management; separates professional partners from vendors who figure things out as they go.

6. Cultural and communication alignment

Operational partnership requires communication fluency. Time zone overlap, English proficiency, responsiveness protocols, and escalation frameworks matter; especially when time-sensitive claims or compliance filings are involved. The best insurance outsourcing relationships function as an extension of your internal team, not as a remote vendor operating in a black box.

7. Industry references and proven outcomes

Ask for case studies from insurers of similar size, line of business, and operational complexity. Request references you can actually speak to. Look for partners who can demonstrate improved workflows, reduced processing times, measurable cost efficiency, and compliance track records.

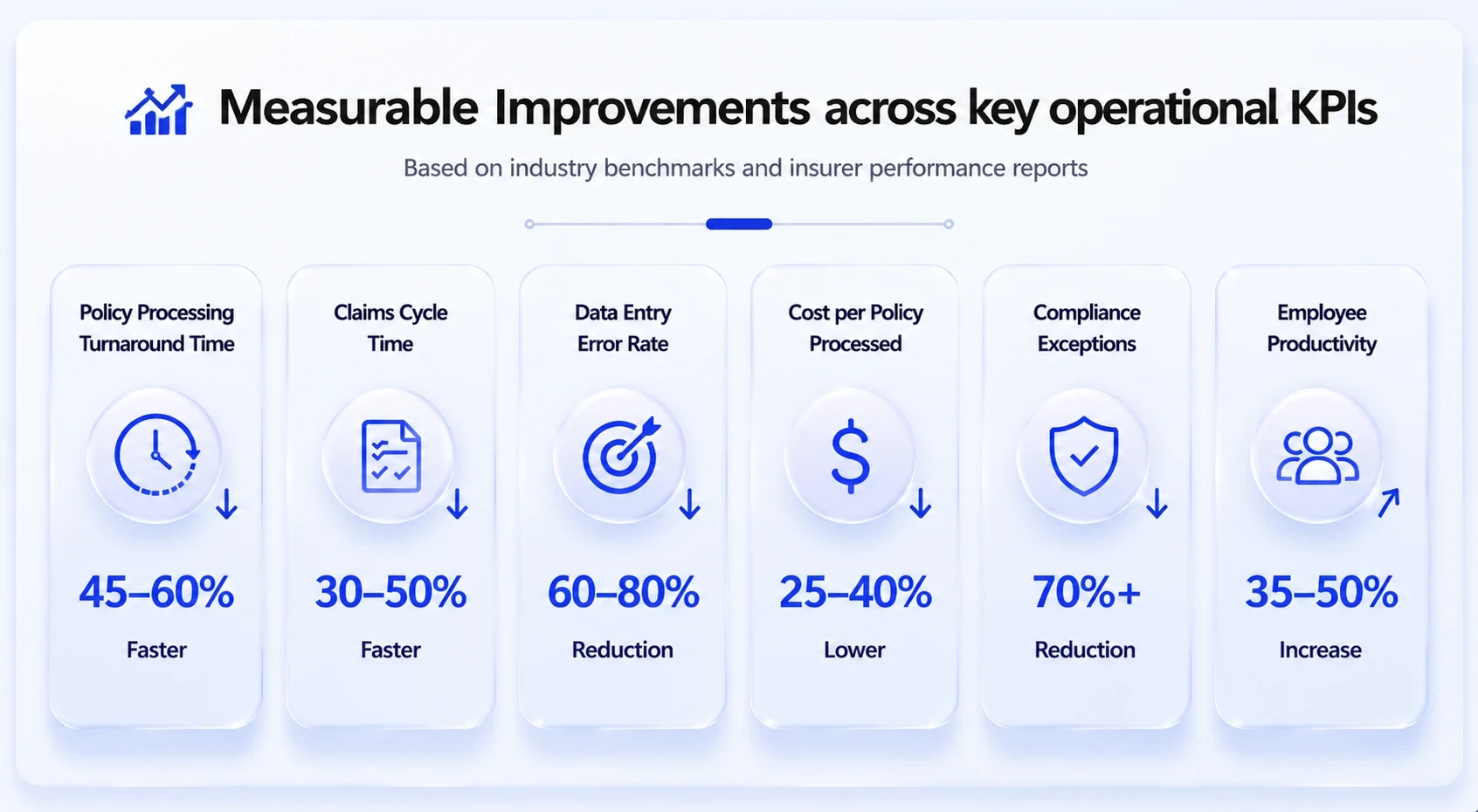

The strategic benefit: What the right partner actually delivers

When the evaluation is done right, the outcomes go far beyond cost reduction. McKinsey research suggests that insurers can improve productivity and reduce operational expenses by up to 40% over the next decade by reimagining processes and embracing digital automation.

That potential only materializes when the outsourcing process is grounded in the right partnership; one built on domain expertise, aligned incentives, and a genuine commitment to operational transformation.

The tangible outcomes you should expect include:

- Accelerated processing velocity across policy, claims, and underwriting workflows

- Error reduction through structured quality control and automation-assisted review

- Compliance assurance without dedicating internal resources to regulatory monitoring

- Cost scalability — paying for capacity as needed rather than carrying fixed overhead

- Strategic bandwidth — freeing your in-house team to focus on growth, client relationships, and product innovation

Red flags to watch for during vendor evaluation

Not every BPO provider that calls itself an insurance specialist is one. Watch for:

- Inability to provide insurance-specific references or case studies

- Generic SLA templates without insurance workflow benchmarks

- No demonstrated integration experience with major insurance platforms

- Vague answers around data security, liability, and compliance protocols

- Over-reliance on offshore labor without quality oversight infrastructure

- No dedicated account management or escalation structure

The future of insurance back-office outsourcing: What's coming

The insurance back-office outsourcing landscape is evolving rapidly. AI-assisted claims triage, natural language processing for document review, predictive underwriting support tools, and real-time compliance monitoring are no longer future possibilities; they're being deployed by leading BPO providers today.

Decision-makers who choose partners aligned with this trajectory are not just solving today's operational problems. They're building the infrastructure for tomorrow's competitive advantage.

The question is no longer whether to outsource your insurance back office. It's who you trust with that transformation.

Why FBSPL stands apart as a strategic back-office partner

FBSPL operates not as a service vendor, but as a strategic consulting partner; purpose-built for the US insurance market.

With deep expertise across insurance back-office support, policy administration, claims management, underwriting assistance, and compliance processing, FBSPL brings the combination that the insurance industry's most complex operational challenges demand: domain-specific knowledge, mature process frameworks, and innovative insurance technology solutions deployed by a team that genuinely understands the American insurance ecosystem.

Whether you're an independent agency, an MGA, or a regional carrier evaluating your operational model, FBSPL offers a structured consultation process to assess your current state, identify transformation opportunities, and build a roadmap aligned with your growth objectives.

Bhavishya Bharadwaj

Bhavishya Bharadwaj is the Digital Marketing Manager at FBSPL, bringing over a decade of experience across insurance, outsourcing, accounting, and digital transformation.

Frequently Asked Questions

Timelines vary based on process complexity and volume, but most transitions take between 4 and 12 weeks, including discovery, knowledge transfer, testing, and phased implementation.