Why virtual assistants have become essential for modern insurance agencies

7 MIN READ/Jun 22, 2026

Summary: Independent insurance agencies face increasing operational pressure as client expectations rise and administrative workloads expand. This blog explores how virtual insurance assistants help agencies improve efficiency, strengthen retention, enhance lead conversion, and scale sustainably without increasing overhead.

Walk into any independent insurance agency today and you'll find the same scene: a handful of producers juggling renewals, certificates of insurance, claims follow-ups, carrier portals, and a CRM that's three steps behind reality. The phones don't stop. The inbox doesn't empty. And the one thing agencies actually need time for; building client relationships and writing new business; keeps getting pushed to "later."

This isn't a staffing problem that more hiring alone can fix. It's a structural mismatch between how insurance agencies are built to operate and how fast the industry around them is changing. That gap is exactly where virtual insurance assistants have moved from a nice-to-have to a operational necessity.

In this blog, we explore how virtual insurance assistants are helping agencies overcome capacity challenges, streamline operations, strengthen client service, and build a scalable foundation for long-term growth.

Insurance is evolving faster than agencies can scale

Insurance has spent the last few years in the middle of a genuine insurance industry digital transformation; not the buzzword version, the operational one. Carriers are automating underwriting, customers expect quote turnaround in minutes rather than days, and back-office work that used to take a full business day now needs to happen in real time.

The data backs up how high the stakes have gotten. McKinsey's analysis of major property-and-casualty carriers found that digitally mature insurers convert online prospects at roughly six times the rate of less digitally advanced competitors; a gap that isn't closing with better software alone, but with a fundamentally different operating model. On the technology adoption side, a Deloitte survey of 200 US insurance executives across the life, annuity, and property and casualty sectors found that 76% had already deployed generative AI capabilities in at least one business function; proof that "wait and see" is no longer a viable strategy for agencies that want to stay competitive.

Meanwhile, the agents actually doing the day-to-day work are stretched thin. Independent agents are responsible for more than 61% of all property and casualty insurance policies written in the US, yet just 56% of personal lines agents and 57% of commercial lines agents say their carriers are meeting even their foundational needs, according to J.D. Power's 2025 U.S. Independent Agent Satisfaction Study, developed with the Independent Insurance Agents & Brokers of America (source). Agencies are carrying the weight of the industry's growth without proportional support; which is precisely the vacuum virtual support in insurance was built to fill.

Where agency operations begin to struggle

Talk to agency principals long enough and the same friction points surface every time.

- Administrative overload: Policy checking, endorsements, certificate issuance, and data entry consume hours that producers should be spending on relationships and renewals.

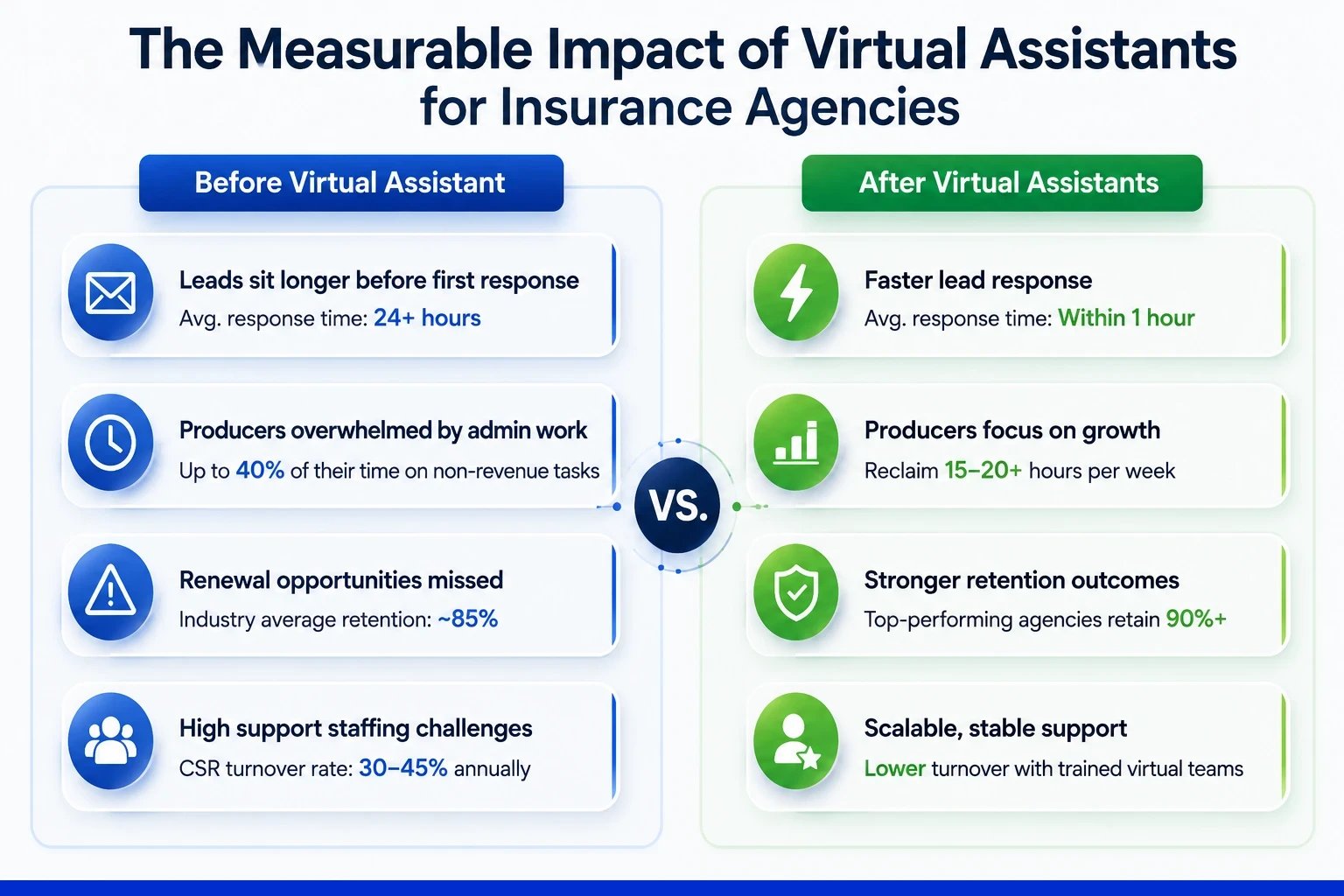

- Inconsistent lead follow-up: Leads go cold not because they weren't good leads, but because nobody had bandwidth to call within the golden hour.

- Renewal and retention gaps: Renewal reminders, re-quotes, and policy reviews fall through the cracks during peak season, putting recurring revenue at risk.

- Compliance and documentation pressure: E&O exposure climbs every time a form is filed late, a policy change is mis-entered, or a client communication isn't logged properly.

- Talent scarcity: Experienced CSRs and account managers are hard to find, expensive to retain, and even harder to scale quickly when growth accelerates.

None of these are technology problems in isolation; they're capacity problems. And capacity is exactly what a virtual assistant for insurance agents is designed to restore.

What a virtual insurance assistant actually does

A virtual insurance assistant isn't a generic admin hire. It's a trained, insurance-literate support resource that plugs directly into an agency's existing systems; AMS platforms, carrier portals, CRMs, and quoting tools; to handle the operational layer of the business. That typically includes policy checking and endorsements, certificate of insurance issuance, new business and renewal data entry, claims status follow-up, quote preparation, client communication, and CRM hygiene.

The distinction matters: this isn't about offloading work to someone unfamiliar with insurance terminology or compliance requirements. It's about embedding a capable extension of the team who understands binders, declarations pages, and carrier-specific workflows from day one.

Key benefits of virtual insurance support

The appeal goes well beyond cost savings, though that's often the entry point.

- Lower fixed overhead: Agencies pay for productive hours, not desks, benefits, or downtime; a meaningfully different cost structure than a full-time in-house hire.

- Faster scaling: Support capacity can expand ahead of a busy renewal season or new book of business without a lengthy hiring cycle.

- Sharper producer focus: When administrative drag is removed, producers spend more of their week on advisory conversations and closing; the work that actually grows the agency.

- Stronger retention outcomes: Consistent renewal reminders and policy reviews, executed on schedule every time, protect the recurring premium base.

- Extended coverage hours: Distributed teams can support client communication and follow-up beyond a single time zone's 9-to-5.

This is the practical answer to a question more agency owners are asking out loud: not "should we adopt technology," but "who actually runs the operational engine while we focus on growth?"

How virtual assistants improve lead conversion

Lead generation in insurance rarely fails at the top of the funnel; it fails in the follow-up. Prospects request quotes, fill out forms, or call in, and then sit untouched while the team handles whatever crisis is loudest that day.

This is where virtual assistants help generate leads in a very concrete way: by owning the follow-up cadence that producers don't have time to maintain. That means same-day callbacks, structured nurture sequences for prospects who aren't ready to buy yet, accurate CRM tagging so nothing slips between stages, and appointment-setting that puts qualified conversations directly onto a producer's calendar. The lead source doesn't change; the conversion discipline does.

Building a scalable agency with the right virtual support

As agencies expand their use of virtual support, selecting the right partner becomes just as important as deciding to outsource in the first place. Agency leaders should carefully evaluate how client data is protected, whether the provider maintains appropriate business insurance and liability coverage, how confidentiality and NDA requirements are handled, and how compliance with state-specific insurance regulations is managed. Because virtual assistants often work with sensitive policy information and personally identifiable data, these considerations should be approached with the same rigor applied to any critical operational partnership.

When implemented thoughtfully, virtual support does more than alleviate administrative burden. It enables agencies to operate with the discipline, consistency, and responsiveness typically associated with much larger organizations. Standardized workflows, dependable follow-up, and expanded operational capacity allow teams to focus on higher-value activities such as strengthening carrier relationships, improving client experiences, and driving growth initiatives.

The agencies gaining a competitive advantage today are not always the largest; they are the ones building scalable operating models that combine internal expertise with specialized external support. With the right virtual partner in place, agencies can preserve their agility while developing the infrastructure needed to sustain long-term success.

Where FBSPL fits into the picture

This is the exact gap FBSPL was built to close. Rather than functioning as a transactional outsourcing vendor, FBSPL operates as a strategic consulting partner for insurance agencies navigating growth, compliance complexity, and the broader shift toward digital, distributed operations. The work centers on designing the right support model for each agency; policy servicing, lead follow-up, renewal management, or back-office processing; and building it into a sustainable operational backbone rather than a stopgap.

Bhavishya Bharadwaj

Bhavishya Bharadwaj is the Digital Marketing Manager at FBSPL, bringing over a decade of experience across insurance, outsourcing, accounting, and digital transformation.

Frequently Asked Questions

The onboarding timeline varies by provider and scope of work, but most agencies can integrate a virtual insurance assistant within a few weeks through structured training and workflow alignment.