7 MIN READ/Jul 08, 2026

Summary: Discover how process optimization helps insurance organizations eliminate inefficiencies, streamline workflows, reduce operational costs, and improve customer experiences. This blog explores proven methods, implementation strategies, key business benefits, and best practices for building scalable, high-performing insurance operations.

Every insurance leader has felt it: a renewal that should take two days stretching into two weeks, an underwriter re-keying the same submission data three different systems demand, a claims adjuster chasing down a document that should have arrived automatically. None of this is a talent problem. It's a process problem; and in an industry where margins are won or lost in the back office, it's quietly the most expensive problem insurers have.

For carriers, MGAs, wholesalers, and agencies, process optimization isn't just about improving efficiency; it's about building operations that support sustainable growth instead of increasing complexity. This piece breaks down what insurance process optimization actually means, why it matters more in 2026 than ever before, and how leading organizations are implementing it; methodically, not magically.

Process optimization is the systematic redesign of workflows; policy administration, underwriting, claims, endorsements, renewals, compliance; to remove friction, reduce manual touchpoints, and shorten cycle times without sacrificing accuracy or compliance. It sits at the intersection of people, technology, and workflow design.

This is distinct from simply "adding automation." Automating a broken process just makes the mess move faster. Real optimization starts with mapping the current state, identifying where value is actually created versus where effort is wasted, and then redesigning the workflow before layering in technology like RPA, AI-driven data extraction, or straight-through processing (STP) rules.

For insurance specifically, this touches nearly every operational domain:

Insurance has entered a phase where premium growth alone no longer guarantees profitability. According to Deloitte's 2026 Global Insurance Outlook, the industry is shifting from a prolonged hard market into one defined by margin pressure and slower premium growth, with the US combined ratio projected to worsen from 97.2% in 2024 to 98.5% in 2025 and 99% in 2026 as claims costs and competitive pressure rise.

That single data point explains why operational discipline has moved from a "nice to have" to a board-level priority. When pricing tailwinds soften, the only lever left that an organization fully controls is how efficiently it operates.

McKinsey's Global Insurance Report 2025 reinforces this: across both soft- and hard-market cycles, the majority of an insurer's financial performance is driven not by where it operates, but by how it operates; meaning execution and operational capability matter more than portfolio strategy or geography. In other words: insurers competing on execution; not just pricing or product; are the ones set up to win the next decade.

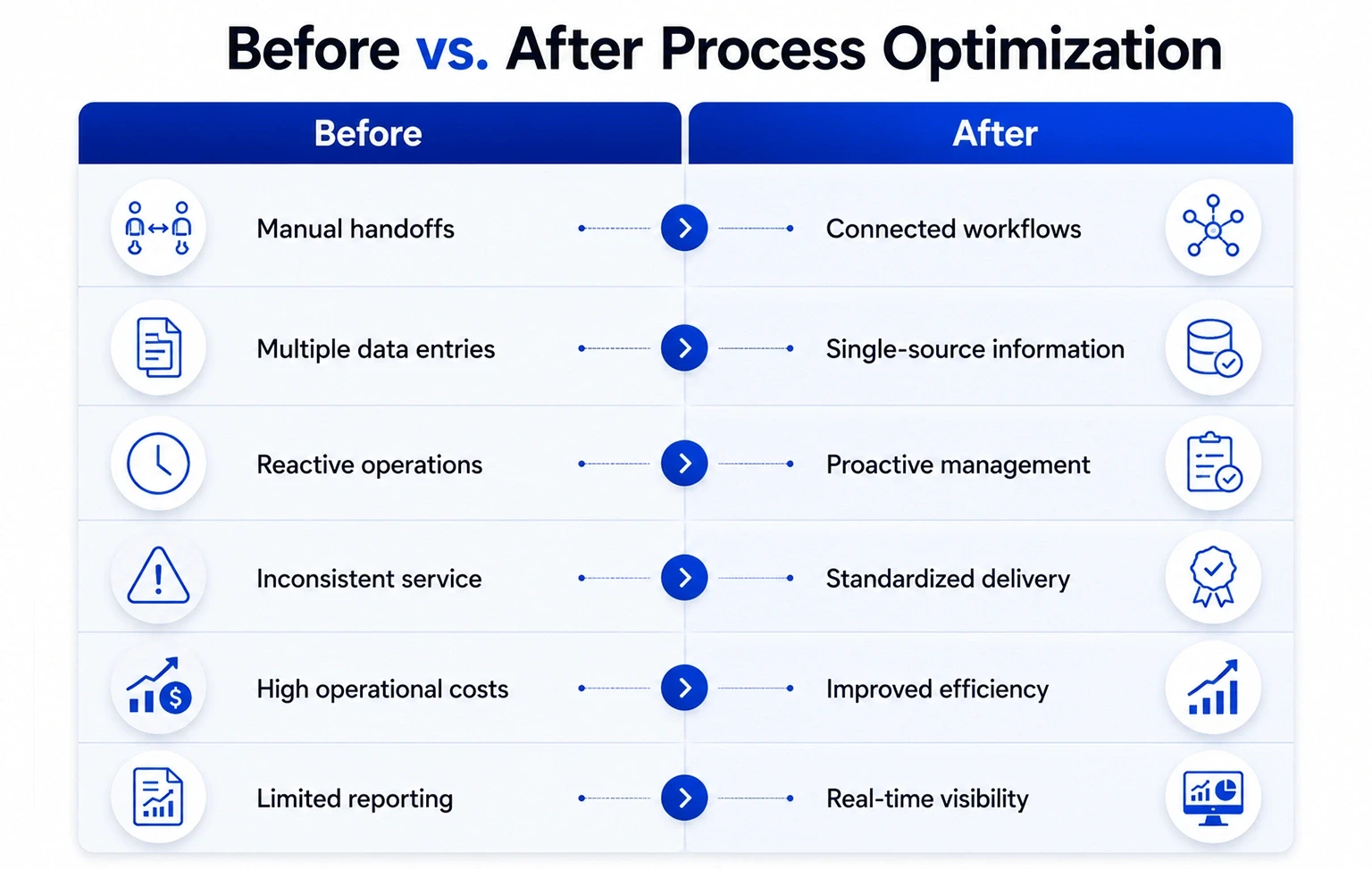

Before looking at solutions, it's worth naming the problems plainly, because they compound quietly:

When done properly, process optimization delivers compounding returns across the organization, not just isolated efficiency wins:

Streamlined underwriting and claims workflows directly shorten quote turnaround, endorsement processing, and claims settlement; improving broker and policyholder satisfaction, which increasingly drives retention.

Removing redundant manual steps reduces labor cost per transaction, which matters enormously as combined ratios tighten industry-wide.

Standardized, rules-driven workflows catch errors before they become costly downstream problems; misclassified risks, incorrect billing, or claims leakage.

Optimized processes let organizations absorb higher policy volume and business growth without a linear increase in staffing costs; a critical advantage in a tight talent market.

Structured, auditable workflows with built-in quality controls make regulatory audits and licensing reviews far less disruptive.

Perhaps the most strategic benefit: when routine servicing and processing tasks are streamlined or delegated, experienced staff can shift toward risk advisory, account rounding, and relationship-building; the activities that actually grow the book of business.

Document the actual workflow; not the one described in the training manual, but what really happens end-to-end. Identify handoffs, bottlenecks, and manual touchpoints. This diagnostic step is where most transformation efforts either succeed or quietly fail before they begin.

Not every process needs immediate attention. Prioritize workflows with high transaction volume and high manual burden; typically policy checking, certificate issuance, endorsements, and FNOL intake; where small improvements produce outsized returns.

Automation applied to an inconsistent process simply automates the inconsistency. Standardizing rules, templates, and decision criteria first ensures technology investments actually compound value rather than just moving the same friction faster.

This is where AI-driven document processing, robotic process automation (RPA), and straight-through processing rules earn their place; not as a wholesale replacement for expertise, but as tools that absorb repetitive, rules-based work. Accenture's research on insurance underwriting reflects this shift: senior underwriting executives expect AI adoption to jump from roughly 14% today to 70% within the next three years, and a large majority believe these tools will create new, higher-value roles rather than simply eliminating existing ones. The pattern across the industry is consistent: technology augments human judgment in underwriting and claims; it doesn't replace the need for it.

Every optimized process needs built-in checkpoints; validation rules, exception flags, audit trails; paired with clear KPIs: turnaround time, cost per transaction, error rate, and compliance adherence. Without measurement, "optimization" becomes anecdotal rather than provable.

Insurance regulation, product complexity, and customer expectations keep shifting. The organizations that sustain an operational edge revisit and refine their workflows on a regular cadence rather than treating optimization as a single initiative with an end date.

The insurers, MGAs, and agencies that will lead over the next several years won't necessarily be the ones with the boldest growth strategy or the most aggressive pricing. They'll be the ones who've quietly, methodically rebuilt how work actually gets done; shortening cycle times, tightening accuracy, and freeing their most experienced people to focus on judgment-intensive work instead of paperwork.

This is precisely where a strategic operations partner adds value that goes beyond simple task execution. At FBSPL, we work alongside insurance carriers, MGAs, wholesalers, and agencies as an extension of their operations; helping diagnose where workflows break down, redesigning processes around measurable outcomes, and applying the right blend of skilled talent and technology to make efficiency sustainable, not just a one-time fix.

Bhavishya Bharadwaj is the Digital Marketing Manager at FBSPL, bringing over a decade of experience across insurance, outsourcing, accounting, and digital transformation.

Frequent bottlenecks, repetitive manual tasks, inconsistent workflows, rising operational costs, delayed service delivery, and increasing customer complaints are common indicators that existing processes need optimization.